Some Known Questions About Paul B Insurance.

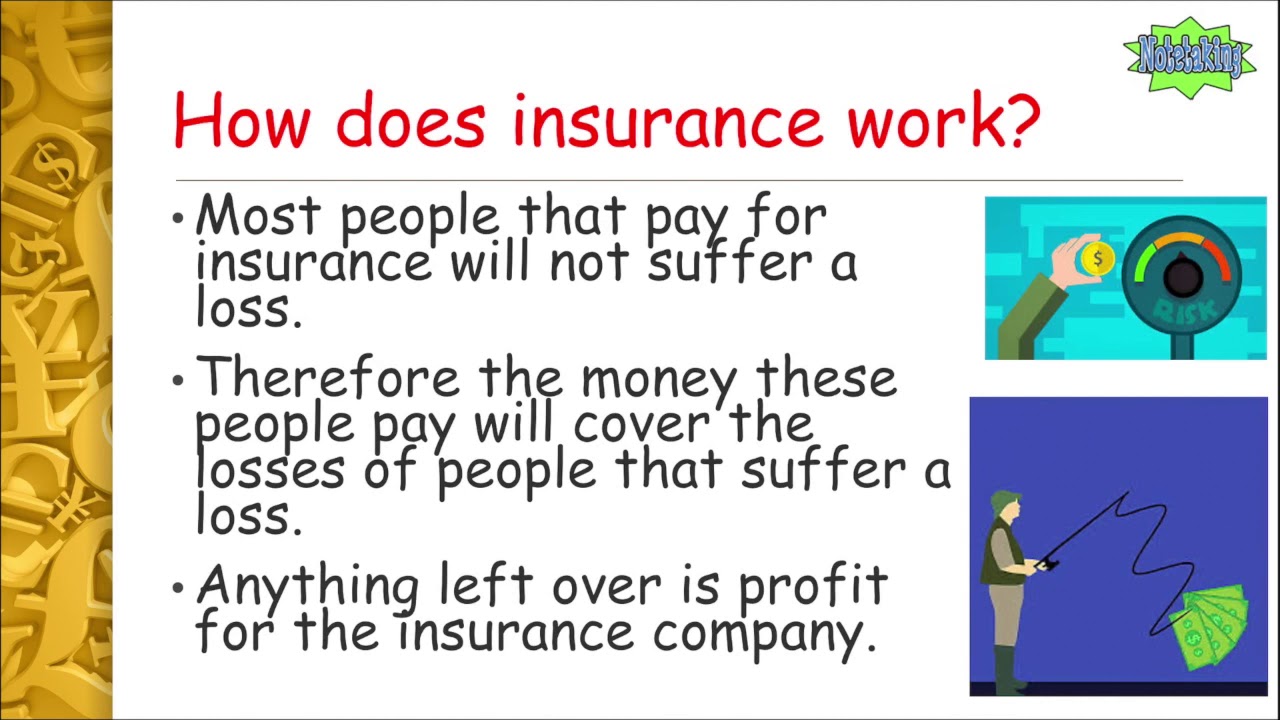

The idea is that the cash paid out in claims gradually will be much less than the overall premiums accumulated. You might seem like you're throwing cash out the window if you never ever submit an insurance claim, but having item of mind that you're covered in case you do experience a substantial loss, can be worth its weight in gold.

Picture you pay $500 a year to insure your $200,000 house. You have ten years of making payments, and you've made no cases. That comes out to $500 times ten years. This implies you have actually paid $5,000 for home insurance policy. You begin to wonder why you are paying so much for absolutely nothing.

Because insurance is based on spreading the risk among numerous individuals, it is the pooled money of all people spending for it that permits the business to construct properties as well as cover claims when they occur. Insurance policy is a business. Although it would certainly behave for the companies to simply leave rates at the same degree all the time, the reality is that they need to make enough cash to cover all the potential cases their policyholders might make.

All about Paul B Insurance

just how a lot they entered costs, they must modify their rates to earn money. Underwriting changes and rate rises or decreases are based upon results the insurance provider had in past years. Depending on what firm you acquire it from, you may be managing a restricted agent. They market insurance policy from just one business.

The frontline people you handle when you purchase your insurance policy are the agents and also brokers that represent the insurer. They will certainly discuss the type of products they have. The restricted agent is an agent of only one insurance provider. They an aware of that firm's products or offerings, yet can not speak towards various other business' policies, rates, or item offerings.

They will have accessibility to greater than one firm and should understand about the array of products supplied by all the companies they stand for. There are a few crucial concerns you can ask yourself that may help you determine what sort of protection you need. Just how much risk or loss of cash can you presume by yourself? Do you have the cash to cover your prices or financial obligations if you have an accident? What concerning if your residence or vehicle is wrecked? Do you have the savings to cover you if you can't work as a result of an accident or disease? Can you pay for greater deductibles in order to lower your prices? Do you have unique needs in your life that need additional protection? What problems you most? Plans can be customized to your needs as well as recognize what you are most concerned regarding safeguarding.

Getting The Paul B Insurance To Work

The insurance you require differs based upon where you go to in your life, what sort of possessions you have, and also what your long-term objectives as well as duties are. That's why it is important to put in the time to discuss what you desire out of your policy with your representative.

If you secure a car loan to buy an automobile, and after that something happens to the vehicle, gap insurance coverage will repay any type of section of your car loan that typical automobile insurance does not cover. Some lending institutions need their customers to carry void insurance policy.

The main function of life insurance coverage is to give money for your beneficiaries when you pass away. Depending on the kind of policy you have, life insurance coverage can cover: Natural deaths.

Paul B Insurance Things To Know Before You Get This

Life insurance coverage covers the life of the guaranteed person. Term life insurance policy covers you for a period of time selected at acquisition, such as 10, 20 or 30 years.

If you do not die during that time, no person gets paid. Term life is prominent due to the fact that it provides big payments at a reduced cost than long-term life. It additionally provides protection for an established variety of years. There are some variations of normal term life insurance policy policies. Convertible policies enable you to transform them to permanent life policies at a higher premium, enabling longer and also possibly much more versatile protection.

Long-term life insurance policy plans develop cash money worth as they age. A part imp source of the premium payments is included to the money value, which can earn rate of interest. their explanation The cash worth of whole life insurance plans grows at go to website a set rate, while the cash value within universal policies can change. You can make use of the cash worth of your life insurance coverage while you're still alive.

Examine This Report on Paul B Insurance

If you compare average life insurance policy rates, you can see the distinction. For instance, $500,000 of whole life insurance coverage for a healthy 30-year-old woman expenses around $4,015 yearly, usually. That same level of insurance coverage with a 20-year term life plan would cost a standard of concerning $188 every year, according to Quotacy, a brokerage company.

Variable life is one more irreversible life insurance option. It's an alternative to whole life with a fixed payout.

Here are some life insurance basics to help you better recognize just how coverage functions. For term life plans, these cover the price of your insurance policy as well as administrative costs.